Summary

A balanced investment strategy in today’s market blends diversification, disciplined asset allocation, and risk management rather than chasing short-term trends. Investors often combine stocks, bonds, cash, and alternative assets while adjusting for age, goals, and market conditions. The goal is steady long-term growth with controlled downside risk, helping portfolios remain resilient through inflation, interest rate shifts, and economic uncertainty.

Building wealth today is not about predicting the next hot stock or timing every market move. It’s about constructing a portfolio that can navigate uncertainty, absorb shocks, and still grow over time.

Over the past several years, investors have faced unusually complex conditions. Inflation surged to multi-decade highs in 2022, interest rates climbed rapidly, and both stocks and bonds experienced volatility. According to data from the Federal Reserve and Bureau of Labor Statistics, inflation pressures and rate hikes have reshaped the traditional investment landscape.

In this environment, the concept of a balanced investment strategy has become more important than ever. Rather than relying on a single asset class, balanced portfolios distribute risk across multiple investments that respond differently to economic changes.

For most long-term investors, the objective is simple: participate in growth while protecting against large losses that could derail financial goals.

Why Balanced Investing Matters More in Today’s Market

Markets historically move through cycles of expansion, slowdown, recovery, and correction. However, the past decade has been unusual because ultra-low interest rates pushed many investors heavily toward stocks.

When interest rates rose sharply beginning in 2022, bonds—which had provided little yield for years—suddenly became attractive again. Meanwhile, stock market volatility reminded investors why diversification matters.

Balanced investing aims to address three realities:

- Markets are unpredictable

- Different assets perform well at different times

- Risk management is essential for long-term success

According to long-term research from Morningstar and Vanguard Group, diversified portfolios historically experience smaller drawdowns than portfolios concentrated in a single asset class.

For example, during major downturns such as the 2008 Global Financial Crisis, diversified portfolios generally recovered faster than portfolios heavily concentrated in equities.

Balanced investing is less about maximizing returns in any single year and more about creating consistency across decades.

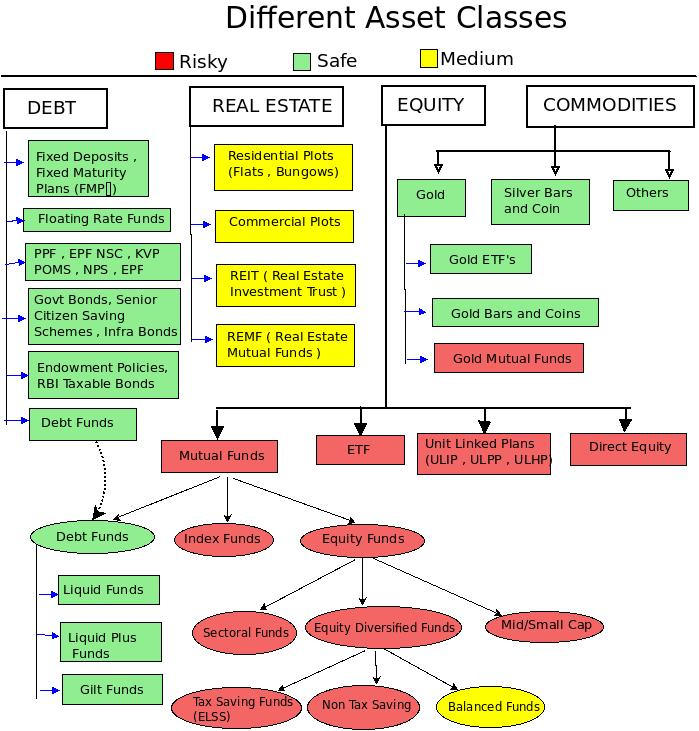

Core Components of a Balanced Investment Portfolio

A balanced portfolio typically includes several categories of assets, each playing a specific role.

Stocks provide growth potential. Bonds offer stability and income. Cash provides liquidity and optionality. Alternative assets can help hedge against inflation or market stress.

A typical diversified portfolio may include:

- Domestic stocks for economic growth exposure

- International stocks for global diversification

- Investment-grade bonds for income and stability

- Treasury securities for safety during downturns

- Cash or money market funds for liquidity

- Alternative assets such as REITs or commodities

The exact mix depends on the investor’s time horizon, financial goals, and tolerance for volatility.

For example, a younger investor with decades before retirement may allocate more toward equities, while someone approaching retirement may shift toward income-producing assets.

The Role of Asset Allocation

Asset allocation is widely considered the most important driver of long-term investment outcomes.

Studies cited by institutional firms such as BlackRock and Fidelity Investments suggest that allocation decisions often explain the majority of portfolio performance variability over time.

Instead of focusing on individual stock picks, balanced strategies prioritize how capital is distributed across asset classes.

Common allocation models include:

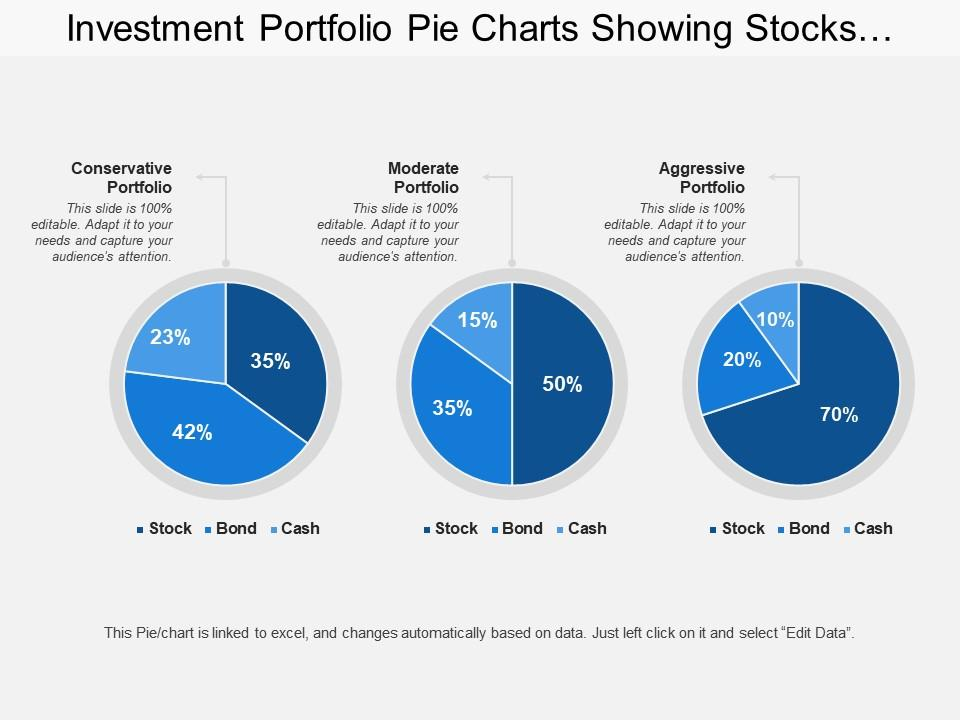

Conservative allocation

- 30–40% stocks

- 50–60% bonds

- 10% cash

Moderate balanced allocation

- 50–60% stocks

- 30–40% bonds

- 5–10% cash

Growth-oriented allocation

- 70–80% stocks

- 15–25% bonds

- small cash reserve

These models are starting points rather than strict rules.

In practice, portfolios evolve as economic conditions and personal circumstances change.

How Interest Rates Are Changing Portfolio Construction

One of the biggest shifts affecting balanced portfolios today is the return of meaningful bond yields.

For much of the 2010s, yields on U.S. Treasury securities remained extremely low. That meant investors seeking returns often moved heavily into equities.

Today, bonds once again play a meaningful role.

For example:

- U.S. Treasury yields have periodically exceeded 4–5% in recent years.

- Short-term Treasury bills provide relatively low-risk income.

- High-quality bonds can act as ballast during equity volatility.

Institutions like J.P. Morgan Asset Management emphasize that the “60/40 portfolio” — 60% stocks and 40% bonds — may regain relevance as bond yields normalize.

Balanced portfolios today often include a broader mix of fixed-income assets such as:

- Treasury bonds

- corporate bonds

- municipal bonds

- short-duration bond funds

This diversification can help stabilize portfolio performance.

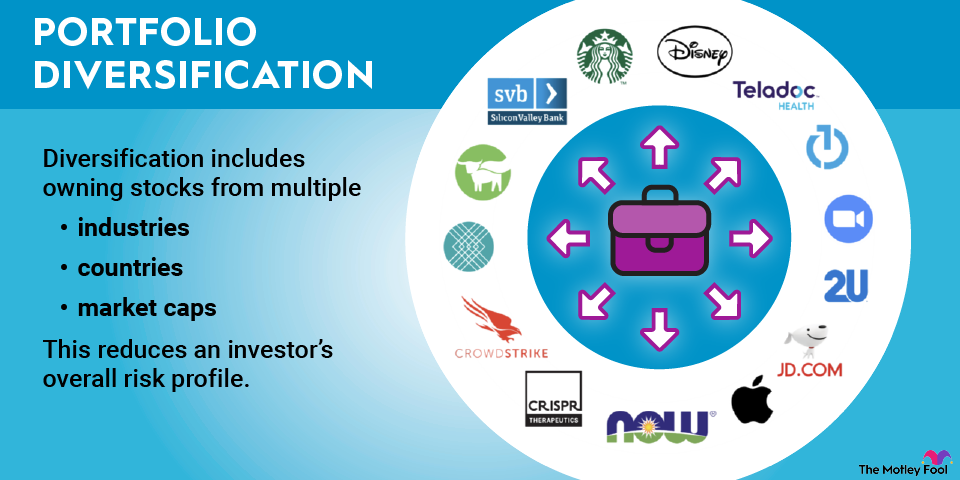

Diversification Beyond Stocks and Bonds

Another modern element of balanced investing is the inclusion of alternative assets.

While not appropriate for every investor, certain alternatives can help reduce portfolio correlation.

Examples include:

- Real estate investment trusts (REITs)

- Commodities or commodity funds

- Infrastructure funds

- Gold or precious metals

During periods of high inflation or geopolitical uncertainty, these assets sometimes behave differently from traditional stocks and bonds.

However, alternatives should generally remain a smaller allocation within a diversified portfolio.

The Importance of Rebalancing

Balanced investing is not a one-time decision.

Markets move constantly, causing portfolio allocations to drift.

For example, if stocks perform strongly for several years, they may grow to represent a much larger portion of a portfolio than originally intended.

Rebalancing restores the target allocation.

Investors typically rebalance:

- annually

- semi-annually

- or when allocations drift beyond certain thresholds

Rebalancing accomplishes two important goals:

- It keeps risk aligned with the investor’s plan

- It enforces discipline by trimming overperforming assets and adding to underperforming ones

This process prevents portfolios from becoming unintentionally concentrated in a single area.

A Real-World Example of a Balanced Portfolio

Consider a hypothetical investor in their early 40s saving for retirement in 20–25 years.

Their balanced portfolio might look like this:

- 45% U.S. stock index funds

- 20% international equities

- 25% bond funds

- 5% real estate investment trusts

- 5% cash or short-term Treasuries

This portfolio seeks growth through equities while maintaining stability through bonds and liquidity.

During strong equity markets, stocks drive returns. During downturns, bonds and cash help cushion losses.

Over long periods, this balanced approach can produce smoother performance than an equity-only portfolio.

Behavioral Discipline: The Often Overlooked Factor

Even the best portfolio strategy can fail if investors react emotionally to market volatility.

According to investor behavior studies by Dalbar, many investors underperform the broader market because they buy during market excitement and sell during downturns.

Balanced portfolios help mitigate this behavioral risk.

When portfolios are diversified, declines are often less severe than all-equity portfolios, making it psychologically easier for investors to remain invested.

Consistency, patience, and adherence to a long-term plan are essential components of successful investing.

Questions Investors Commonly Ask About Balanced Strategies

What is considered a balanced investment portfolio?

A balanced portfolio typically includes a mix of equities, fixed income, and cash equivalents designed to balance growth potential with risk management.

Is the traditional 60/40 portfolio still relevant?

Many analysts believe it may regain relevance as bond yields rise, although modern portfolios often include broader diversification beyond just stocks and bonds.

How often should a portfolio be rebalanced?

Most financial advisors recommend reviewing allocations annually or whenever asset classes drift significantly from target levels.

Can balanced portfolios outperform stock-only portfolios?

In strong bull markets, stock-heavy portfolios may outperform. However, balanced portfolios often provide smoother returns and lower drawdowns over full market cycles.

Are bonds still useful in a balanced portfolio?

Yes. Bonds provide income, reduce volatility, and often perform better than stocks during economic slowdowns.

Should younger investors use balanced portfolios?

Younger investors may allocate more toward equities but still benefit from diversification across asset classes.

How much cash should be included in a portfolio?

Many balanced portfolios maintain 3–10% in cash or cash equivalents to manage liquidity and take advantage of opportunities.

Do balanced portfolios protect against inflation?

They can help, particularly when including assets like equities, real estate, or commodities that historically respond to inflation.

Are index funds useful for balanced strategies?

Yes. Many investors use low-cost index funds to build diversified portfolios efficiently.

Can balanced portfolios work during volatile markets?

Yes. Diversification and asset allocation are specifically designed to manage volatility and reduce large losses.

Building Stability While Still Pursuing Growth

Balanced investing recognizes a fundamental truth about financial markets: no single asset class wins every year.

Stocks may lead during economic expansion, bonds may outperform during recessions, and alternative assets may shine during inflationary periods.

By spreading investments across multiple categories, balanced portfolios create resilience.

For long-term investors, this resilience can be far more valuable than attempting to predict the next market trend.

Key Ideas to Remember When Building a Balanced Portfolio

- Diversification reduces risk concentration

- Asset allocation is a primary driver of outcomes

- Bonds are becoming relevant again as yields rise

- Rebalancing maintains discipline

- Behavioral consistency is critical to long-term success

The Strategic Balance That Defines Long-Term Investing

Balanced investing is less about predicting markets and more about preparing for them.

A portfolio built around diversification, disciplined allocation, and periodic rebalancing is designed to endure multiple economic environments—from inflation and rising interest rates to recessions and bull markets.

For long-term investors, stability combined with steady growth often proves more valuable than chasing short-term returns.

Snapshot of the Core Lessons

- Balanced portfolios combine growth assets with stabilizing investments

- Asset allocation decisions often matter more than individual stock picks

- Bonds are regaining importance as yields rise

- Diversification across asset classes improves resilience

- Regular rebalancing maintains intended risk levels

- Behavioral discipline is essential during market volatility