Summary

Smart investing isn’t about chasing trends or predicting the next big stock. The principles that have helped Americans build wealth for decades—diversification, long-term thinking, disciplined risk management, and consistent contributions—remain highly relevant today. Understanding these fundamentals can help individuals navigate market volatility, make more informed decisions, and steadily build financial security over time.

Why Investment Fundamentals Still Matter

Financial markets change constantly. New technologies emerge, investment platforms evolve, and economic conditions shift. Yet the core principles of successful investing have remained surprisingly consistent.

For generations, disciplined investors in the United States have relied on a few foundational ideas: investing regularly, diversifying assets, focusing on long-term growth, and managing risk carefully. These principles have guided individuals through periods of inflation, recessions, technological revolutions, and major market cycles.

According to historical market data from sources such as S&P Dow Jones Indices, the U.S. stock market has delivered an average annual return of roughly 10% over the long term, despite short-term volatility. The key takeaway is not that markets always rise quickly, but that long-term participation has historically rewarded patient investors.

Today’s investment landscape includes more options than ever—ETFs, robo-advisors, cryptocurrency markets, and mobile trading platforms. While these tools change how people invest, the underlying fundamentals remain largely unchanged.

Understanding those fundamentals helps investors make decisions based on logic rather than emotion.

Understanding the Goal of Smart Investing

Before choosing investments, it’s important to clarify the purpose of investing in the first place.

For most Americans, investing serves several long-term goals:

- Building retirement savings

- Protecting purchasing power against inflation

- Growing wealth over decades

- Funding education or major life expenses

- Creating financial independence

Smart investing focuses on aligning investments with these goals rather than reacting to short-term market headlines.

A common mistake new investors make is assuming successful investing requires constant trading. In reality, many professional financial advisors emphasize steady, disciplined strategies that prioritize long-term growth.

For example, someone investing $500 monthly into a diversified retirement portfolio beginning at age 30 could potentially accumulate hundreds of thousands of dollars by retirement, assuming moderate market returns.

The power of investing often comes from time and consistency, not frequent trading.

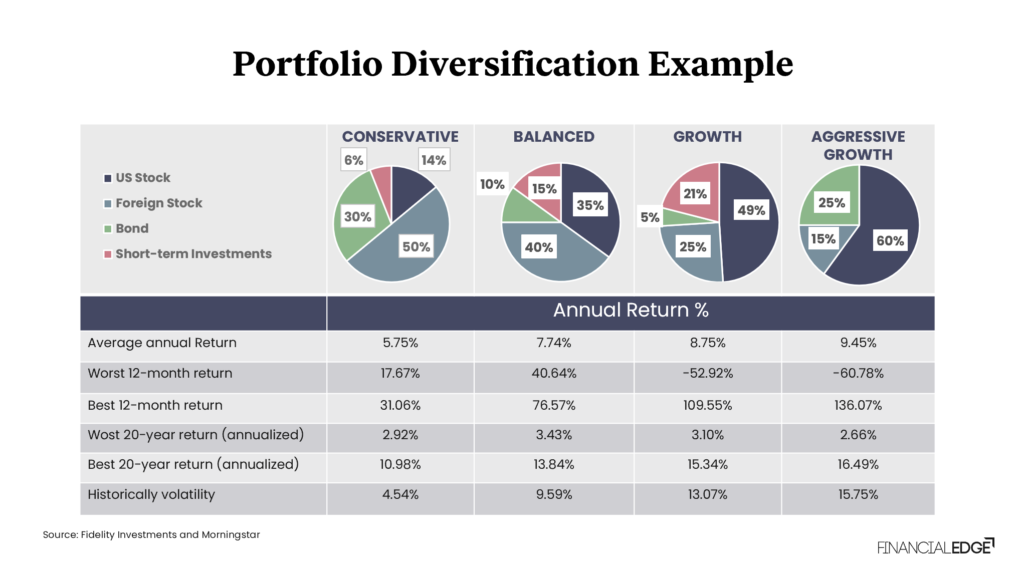

Diversification: One of the Most Reliable Risk Controls

Diversification remains one of the most widely recommended investment strategies.

Simply put, diversification means spreading investments across different asset types to reduce exposure to any single risk.

When one investment performs poorly, others may help balance the portfolio.

Typical diversified portfolios often include:

- U.S. stocks

- International stocks

- Bonds

- Real estate investments

- Cash or short-term instruments

Many investors achieve diversification through index funds or exchange-traded funds (ETFs), which track large segments of the market.

For instance, an investor who owns an S&P 500 index fund holds shares in 500 major U.S. companies across multiple industries. This reduces the risk associated with owning a single company’s stock.

Diversification does not eliminate risk, but it helps reduce the impact of unexpected market events.

The Importance of Long-Term Thinking

Short-term market movements can be unpredictable. News headlines often focus on daily fluctuations, but successful investors tend to focus on longer time horizons.

Historically, markets have experienced numerous temporary declines:

- The dot-com crash in the early 2000s

- The financial crisis of 2008

- The pandemic-related market drop in 2020

Despite these downturns, markets have historically recovered and continued growing over time.

Long-term investors typically follow a strategy sometimes referred to as “buy and hold.” Instead of attempting to time the market, they remain invested through cycles.

Financial research repeatedly shows that missing just a few of the market’s best-performing days can significantly reduce long-term returns. Investors who stay invested are more likely to capture those recovery periods.

Patience is often one of the most valuable skills in investing.

Consistency: The Quiet Driver of Portfolio Growth

Many investors underestimate the power of consistent contributions.

Regular investing—sometimes called dollar-cost averaging—means investing the same amount of money at regular intervals regardless of market conditions.

This approach offers several advantages:

- It reduces the pressure to predict market timing

- It smooths purchase prices over time

- It encourages disciplined saving habits

For example, a worker contributing to a 401(k) plan every paycheck is practicing a form of dollar-cost averaging. Over years or decades, these contributions compound and can grow significantly.

Consistency also helps investors remain engaged with their financial goals, even during periods when markets feel uncertain.

Managing Risk Without Avoiding Opportunity

Risk is an unavoidable part of investing. However, smart investors focus on managing risk rather than eliminating it entirely.

Risk tolerance varies from person to person and often depends on factors such as age, income stability, and investment timeline.

Younger investors often accept more stock exposure because they have decades to recover from market fluctuations. Those approaching retirement typically shift toward more stable assets like bonds.

Common risk-management strategies include:

- Maintaining a diversified portfolio

- Rebalancing investments periodically

- Adjusting asset allocation based on life stage

- Avoiding excessive concentration in a single investment

Rebalancing is especially important. Over time, certain investments may grow faster than others, causing the portfolio to drift from its original allocation.

Periodic adjustments help maintain the intended risk profile.

The Role of Costs and Fees in Long-Term Investing

Investment costs can significantly influence long-term outcomes.

Even seemingly small fees can compound over time.

For example:

- A 1% annual management fee may appear modest.

- Over decades, however, it can reduce portfolio value by tens of thousands of dollars depending on account size.

Many modern investors therefore favor low-cost index funds and ETFs, which often have expense ratios below 0.10%.

Lower costs allow a larger portion of investment returns to remain in the investor’s account.

Financial advisors often encourage investors to review expense ratios, management fees, and trading costs when selecting funds.

Emotional Discipline: An Often Overlooked Skill

One of the greatest challenges in investing is managing emotions.

Market volatility can trigger fear or excitement that leads to impulsive decisions.

Common emotional mistakes include:

- Selling during market downturns

- Chasing popular investment trends

- Overreacting to financial news

- Attempting to time short-term market moves

Experienced investors often rely on a written investment strategy or financial plan to guide decisions during uncertain periods.

By sticking to a structured plan, investors can reduce the influence of short-term emotions.

How Technology Has Changed Access to Investing

While the fundamentals remain consistent, technology has transformed how Americans invest.

Today’s investors benefit from:

- Commission-free trading platforms

- Automated investing services (robo-advisors)

- Fractional share investing

- Mobile portfolio management tools

- Expanded financial education resources

These innovations have lowered barriers to entry, allowing more individuals to begin investing earlier.

However, easier access also means investors must be cautious about information overload and speculative trading trends.

Technology can enhance investing, but the underlying principles remain the same.

Frequently Asked Questions

What is the most important rule of investing?

Many financial professionals emphasize long-term discipline as the most important principle. Remaining invested through market cycles historically provides better outcomes than reacting to short-term market changes.

How much should someone invest each month?

Financial planners often suggest investing 10–20% of income when possible, though the appropriate amount varies depending on personal finances, debt obligations, and financial goals.

Is diversification really necessary?

Yes. Diversification helps reduce the risk of significant losses from any single investment or sector.

Are index funds good for beginners?

Index funds are widely considered beginner-friendly because they offer built-in diversification and relatively low costs.

Can someone start investing with a small amount?

Yes. Many modern platforms allow investors to begin with small amounts through fractional shares or automated investing services.

How often should a portfolio be rebalanced?

Many investors review allocations once or twice per year, though the appropriate frequency depends on investment strategy.

What role do bonds play in a portfolio?

Bonds can provide stability and income while reducing overall portfolio volatility.

Is it possible to time the stock market successfully?

Consistently timing the market is extremely difficult, even for professional investors.

What is dollar-cost averaging?

Dollar-cost averaging is the practice of investing a fixed amount regularly regardless of market conditions.

Should beginners work with a financial advisor?

Some investors benefit from professional guidance, especially when developing retirement plans or managing complex finances.

Building Wealth With Discipline Over Time

Successful investing rarely depends on predicting the next major market movement. Instead, it often comes from following well-established principles consistently over many years.

Investors who diversify their portfolios, invest regularly, manage costs, and maintain emotional discipline place themselves in a stronger position to benefit from long-term economic growth.

While markets will always experience uncertainty, these enduring fundamentals continue to provide a reliable framework for thoughtful investment decisions.

Core Investing Ideas Worth Remembering

- Long-term investing historically outperforms short-term speculation

- Diversification reduces exposure to individual risks

- Consistent contributions can significantly increase portfolio growth

- Investment costs matter more than many investors realize

- Emotional discipline often separates successful investors from reactive ones

- Technology expands access but does not replace sound strategy