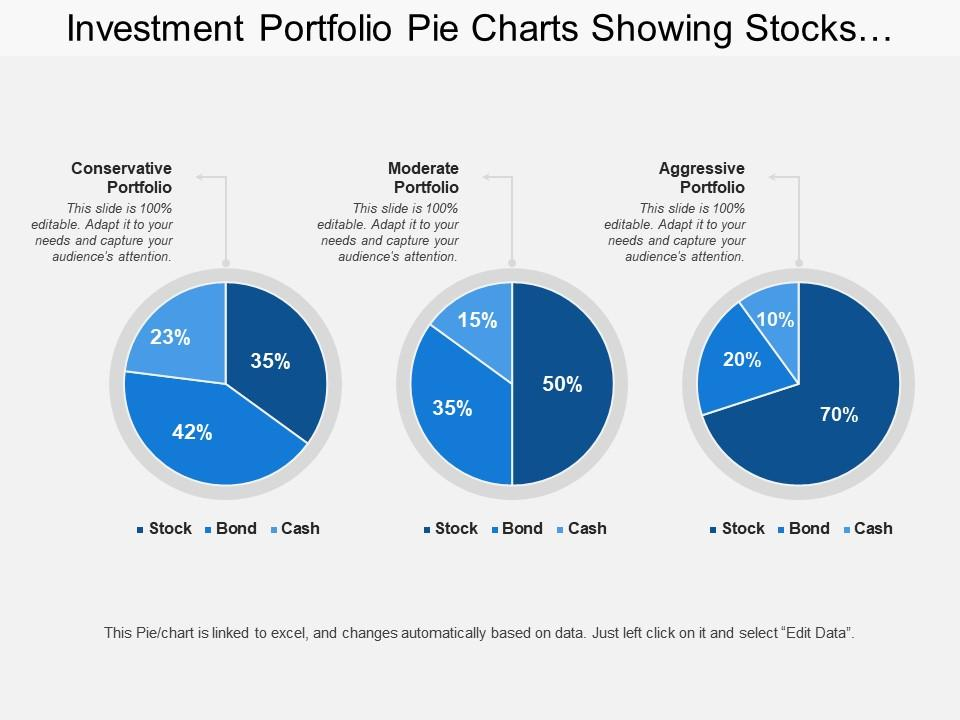

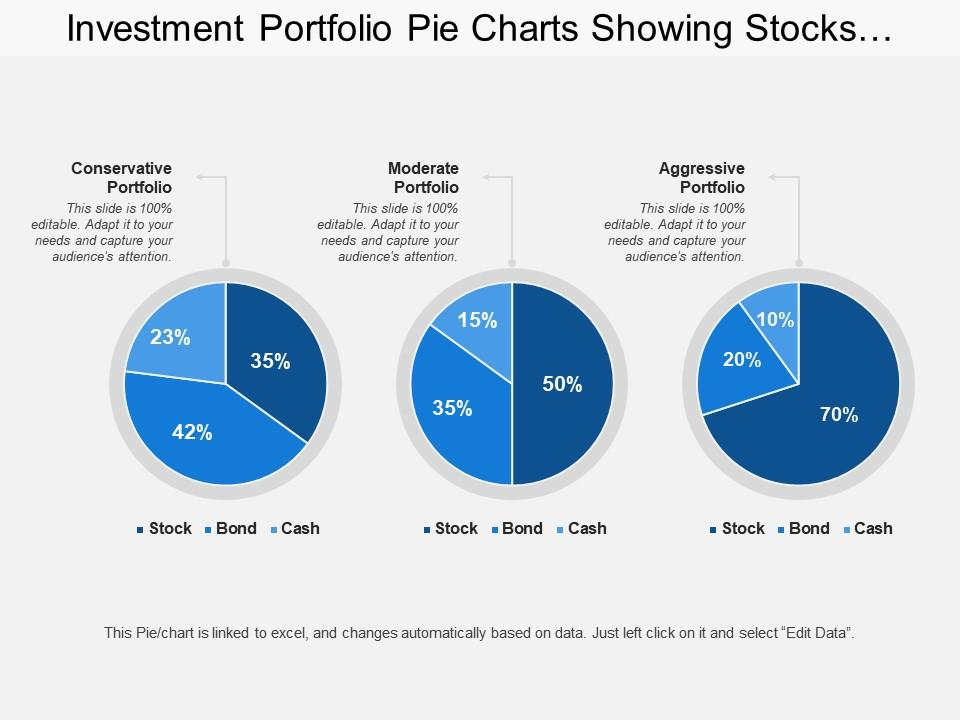

Summary

Diversification remains one of the most reliable strategies in modern investment planning. By spreading capital across different asset classes, sectors, and geographic regions, investors can reduce risk while maintaining growth potential. Today’s diversified portfolios go beyond traditional stocks and bonds, incorporating global markets, alternative assets, and ETFs to create resilient portfolios designed to withstand economic uncertainty and market volatility.

Why Diversification Still Matters in Modern Investing

Diversification is not a new idea. Financial advisors have promoted it for decades, yet its relevance has only increased as financial markets grow more interconnected and complex. At its core, diversification means spreading investments across different assets so that no single market event can severely damage an entire portfolio.

Market history consistently demonstrates the value of diversification. During the 2008 global financial crisis, portfolios heavily concentrated in equities suffered dramatic losses. Investors holding a mix of bonds, commodities, and international assets generally experienced smaller drawdowns and faster recoveries.

Today’s investment environment is shaped by rapid technological change, global economic shifts, inflation cycles, and geopolitical risks. A diversified portfolio helps absorb shocks from these unpredictable forces.

According to research from Morningstar and Vanguard, asset allocation—how investments are divided among asset classes—can explain more than 80% of a portfolio’s long-term performance variability. This underscores why diversification remains central to investment planning.

Understanding the Core Idea Behind Diversification

Diversification works because different assets tend to respond differently to the same economic conditions. When one investment declines, another may rise or remain stable.

For example:

- Stocks often perform well during economic expansion.

- Bonds may provide stability during recessions.

- Commodities can benefit during inflationary periods.

- Real estate can provide both income and long-term appreciation.

When combined strategically, these assets can reduce overall volatility.

However, diversification does not guarantee profits or eliminate losses. Instead, it aims to smooth returns over time, helping investors stay invested through market cycles.

The Evolution of Diversification in the Modern Era

Traditional diversification once meant simply holding a mix of stocks and bonds. Modern investment planning is significantly more sophisticated.

Several trends have reshaped how investors diversify today:

- Expansion of global investment opportunities

- Growth of low-cost exchange-traded funds (ETFs)

- Access to alternative assets for individual investors

- Advanced portfolio analytics and risk modeling

- Increased financial education among retail investors

As a result, diversification strategies today often span multiple dimensions—asset class, geography, industry exposure, and investment style.

Key Asset Classes That Support Diversified Portfolios

A modern diversified portfolio typically includes several major asset classes. Each plays a distinct role in balancing risk and return.

1. Equities (Stocks)

Stocks represent ownership in companies and historically provide the strongest long-term growth potential.

However, stocks also carry higher volatility. Diversifying within equities—across industries, company sizes, and global markets—can reduce risk.

Common equity diversification strategies include:

- Large-cap and small-cap stock exposure

- Growth and value investing styles

- U.S. and international equities

- Sector diversification (technology, healthcare, finance, energy)

2. Fixed Income (Bonds)

Bonds provide income and help stabilize portfolios during equity market downturns.

Investors commonly diversify bond holdings by including:

- U.S. Treasury bonds

- Corporate bonds

- Municipal bonds

- International bonds

- Short- and long-term maturities

Historically, bonds have shown lower volatility than stocks, which helps reduce overall portfolio fluctuations.

3. Real Assets

Real assets include investments tied to physical resources or property. These often perform well during inflationary environments.

Examples include:

- Real estate investment trusts (REITs)

- Commodities such as gold and oil

- Infrastructure investments

- Farmland and timberland

Adding real assets can help protect purchasing power over long time horizons.

Diversification Across Global Markets

One of the most important developments in modern investing is the ability to easily access international markets.

The U.S. represents roughly 60% of global equity market capitalization, meaning significant opportunities exist outside domestic markets.

International diversification can help investors benefit from:

- Economic growth in emerging markets

- Different interest rate environments

- Currency diversification

- Industry exposure not dominant in U.S. markets

For instance, emerging economies in Asia and Latin America often experience faster GDP growth than developed economies, which can create attractive investment opportunities.

However, international investing also introduces additional risks, including currency fluctuations and political instability. Diversification helps balance those risks.

The Role of Alternative Investments

Alternative assets have become increasingly common in diversified portfolios. Once limited to institutional investors, many alternatives are now accessible through ETFs and mutual funds.

These investments often have low correlation with traditional stocks and bonds, meaning their performance may differ significantly from broader markets.

Common alternatives include:

- Private equity funds

- Hedge fund strategies

- Commodities

- Infrastructure investments

- Private real estate

For example, during periods of rising inflation, commodities like oil and metals have historically performed better than traditional financial assets.

However, alternatives can involve higher fees, lower liquidity, and more complex risk profiles, making careful evaluation essential.

Diversification Within Equity Markets

Many investors believe owning multiple stocks automatically creates diversification. In reality, diversification requires exposure across different industries and economic drivers.

Holding ten technology stocks may still create concentrated risk if the technology sector declines.

A well-diversified equity portfolio typically includes exposure to sectors such as:

- Technology

- Healthcare

- Financial services

- Consumer goods

- Energy

- Industrials

- Utilities

Exchange-traded funds (ETFs) have made this type of diversification easier than ever.

For example, a single broad-market ETF tracking the S&P 500 can instantly provide exposure to hundreds of companies across multiple sectors.

How ETFs Transformed Portfolio Diversification

Exchange-traded funds have revolutionized diversification for everyday investors.

ETFs allow investors to buy an entire index, sector, or asset class with a single transaction.

Advantages include:

- Low expense ratios

- Instant diversification

- High liquidity

- Tax efficiency

- Transparency in holdings

Today investors can access ETFs covering virtually every market segment—from U.S. large-cap stocks to global infrastructure or emerging market bonds.

According to the Investment Company Institute, U.S. ETF assets surpassed $8 trillion in 2023, reflecting their growing role in diversified portfolio construction.

Practical Diversification Strategies for Individual Investors

While diversification is widely recommended, implementing it effectively requires thoughtful planning.

Several practical strategies can help investors build diversified portfolios.

Use Broad Market Index Funds

Index funds track large market segments and offer built-in diversification at low cost.

Examples include:

- Total U.S. stock market funds

- Global stock index funds

- Aggregate bond index funds

These funds form the foundation of many long-term portfolios.

Rebalance Regularly

Over time, certain investments grow faster than others, which can unintentionally increase risk.

Rebalancing involves periodically adjusting holdings back to target allocations.

For example:

- Selling some outperforming assets

- Buying underweighted asset classes

This process helps maintain intended diversification.

Diversify Across Time Horizons

Investors can also diversify by investing regularly over time rather than all at once.

Strategies like dollar-cost averaging reduce the risk of investing large sums at unfavorable market moments.

Common Diversification Mistakes

Despite its simplicity, diversification is often misunderstood or poorly executed.

Common mistakes include:

- Over-diversification, which dilutes potential returns

- Holding multiple funds with overlapping holdings

- Ignoring global investment opportunities

- Concentrating heavily in employer stock

- Failing to rebalance portfolios

Another common issue is behavioral bias. Investors often chase recent market winners, unintentionally reducing diversification.

Disciplined asset allocation helps avoid these pitfalls.

Diversification in Retirement Planning

Diversification becomes especially important as investors approach retirement.

At this stage, protecting accumulated wealth becomes just as important as growing it.

Retirement-focused diversification often includes:

- A higher allocation to bonds and income-producing assets

- Dividend-paying stocks

- Inflation-protected securities

- Real estate income sources

This approach helps maintain portfolio stability while generating sustainable income.

Financial planners frequently recommend gradually adjusting asset allocation with age, a strategy commonly known as a glide path.

Why Diversification Remains Timeless

Investment trends come and go—cryptocurrencies, AI stocks, speculative trading—but diversification continues to remain a foundational principle of responsible investing.

Even the most sophisticated institutional investors rely heavily on diversified portfolios.

The reason is simple: markets are unpredictable.

Diversification acknowledges this uncertainty and builds resilience into investment strategies. Rather than attempting to predict which asset will outperform next, diversified portfolios allow investors to participate broadly in economic growth while managing downside risk.

Frequently Asked Questions

What is diversification in investing?

Diversification is the practice of spreading investments across different asset classes, industries, and geographic regions to reduce risk and improve long-term portfolio stability.

Why is diversification important?

Diversification reduces the impact of poor performance in any single investment. It helps smooth returns and lowers overall portfolio volatility.

How many investments should a diversified portfolio have?

There is no fixed number, but many diversified portfolios include exposure to hundreds or even thousands of securities through index funds or ETFs.

Does diversification guarantee profits?

No. Diversification cannot eliminate losses, but it helps reduce the risk of large losses from any single investment.

What is the easiest way to diversify?

Broad-market index funds or ETFs are one of the simplest and most cost-effective ways to achieve diversification.

Should beginners focus on diversification?

Yes. Diversification is especially important for beginners because it reduces reliance on predicting individual stock performance.

Is international diversification necessary?

Many financial experts recommend it because global markets provide additional growth opportunities and reduce reliance on a single economy.

Can diversification reduce returns?

In some cases, diversification may limit extreme gains, but it also reduces the likelihood of severe losses.

How often should investors rebalance?

Many advisors recommend reviewing portfolio allocations once or twice per year.

Are alternative investments necessary for diversification?

Not always. Many investors achieve effective diversification using stocks, bonds, and real assets without complex alternatives.

Building Resilient Portfolios for an Uncertain Future

Diversification continues to shape modern investment planning because it addresses the one certainty in financial markets: uncertainty itself. Investors cannot predict every economic shift, interest rate move, or geopolitical shock. What they can control is how broadly their investments are spread.

By thoughtfully allocating assets across markets, sectors, and asset classes, investors create portfolios designed to endure market cycles rather than react to them. In a world of constant change, diversification remains one of the most practical tools for long-term financial stability.

Key Insights Investors Should Remember

- Diversification spreads risk across different investments

- Asset allocation drives most long-term portfolio performance

- Modern diversification includes global markets and alternative assets

- ETFs have made diversification easier and cheaper

- Regular rebalancing maintains portfolio balance

- Diversification supports both growth and risk management

- Retirement portfolios rely heavily on diversified income sources

- Concentrated investments increase long-term risk exposure