Summary

Long-term investing focuses on steadily building wealth over years or decades rather than chasing short-term gains. Strategies such as diversified portfolios, consistent contributions, and disciplined risk management allow investors to benefit from compounding and market growth. This guide explores practical, real-world approaches Americans use to pursue sustainable long-term investment growth while managing volatility and staying aligned with financial goals.

Why Long-Term Growth Matters in Investing

For most Americans, investing is not about quick profits. It is about building financial security over time—saving for retirement, funding education, or creating generational wealth. Long-term investment strategies aim to capture the natural growth of the economy and financial markets while minimizing the damage caused by short-term volatility.

Historically, this approach has been supported by market data. According to research from Standard & Poor’s, the S&P 500 has delivered an average annual return of roughly 10% before inflation since 1926, despite wars, recessions, and market crashes. The lesson many experienced investors take from this history is clear: time in the market often matters more than timing the market.

Long-term strategies prioritize patience, diversification, and consistency. Instead of reacting emotionally to daily market swings, investors focus on maintaining a disciplined plan designed to work over decades.

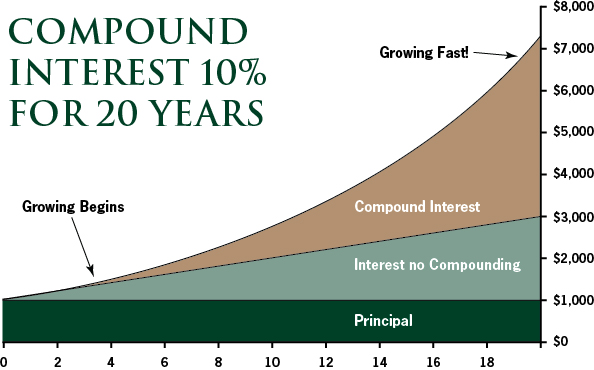

Understanding the Power of Compounding

Compounding is one of the most important drivers of long-term investment growth. It occurs when investment earnings generate their own earnings over time.

A simple example illustrates this effect. Suppose an investor contributes $500 per month to a retirement account earning an average annual return of 7%.

After:

- 10 years: about $86,000

- 20 years: about $260,000

- 30 years: about $610,000

The majority of the growth occurs in the later years as returns begin compounding on previous gains.

This is why long-term strategies emphasize starting early and staying invested. Even modest contributions can grow substantially over several decades when compounded consistently.

Core Investment Approaches Designed for Long-Term Growth

Several investment frameworks are widely used by financial professionals and experienced investors who prioritize sustained growth.

Diversified Portfolio Investing

Diversification spreads investments across different asset classes, industries, and geographic regions. The goal is to reduce the risk associated with any single investment performing poorly.

A typical diversified portfolio might include:

- U.S. stocks

- International stocks

- Bonds

- Real estate investment trusts (REITs)

- Cash equivalents

When one sector experiences a downturn, others may perform better, helping stabilize overall returns.

For example, during the 2008 financial crisis, equities dropped sharply. However, U.S. Treasury bonds gained value, providing some protection for diversified portfolios.

Index Investing

Index investing has become one of the most widely used long-term strategies in the United States.

Instead of trying to outperform the market through active stock picking, index investors purchase funds designed to mirror a market index such as the S&P 500.

This strategy has several advantages:

- Lower management fees

- Broad diversification

- Historically competitive performance

According to data from Morningstar, over 80% of actively managed U.S. equity funds underperform their benchmark indexes over long periods, which is why many long-term investors prefer low-cost index funds.

For retirement savers, index investing often forms the foundation of portfolios held in 401(k)s, IRAs, and taxable brokerage accounts.

Dollar-Cost Averaging

Dollar-cost averaging involves investing a fixed amount of money at regular intervals regardless of market conditions.

For example, someone might invest $300 every two weeks into a retirement account.

This approach offers two practical benefits:

- It removes emotional decision-making

- It automatically buys more shares when prices are lower

Over time, this can help smooth the impact of market volatility.

Many Americans practice dollar-cost averaging through automatic contributions to workplace retirement plans.

Asset Allocation: Balancing Growth and Risk

Asset allocation refers to how investments are divided among asset classes such as stocks, bonds, and alternatives. The right mix depends largely on time horizon and risk tolerance.

A commonly used framework suggests:

- Younger investors: higher stock allocation for growth

- Mid-career investors: balanced mix of stocks and bonds

- Near retirement: more conservative allocation

Stocks historically offer higher growth potential but greater volatility, while bonds tend to provide stability and income.

For instance, a 30-year-old saving for retirement may hold 80–90% equities, while someone nearing retirement might shift toward a 60/40 or 50/50 allocation.

Regular portfolio rebalancing helps maintain the intended allocation as market values change.

The Role of Tax-Advantaged Accounts

Tax efficiency is another key element of long-term investing.

U.S. investors often use tax-advantaged accounts such as:

- 401(k) plans

- Traditional IRAs

- Roth IRAs

- Health Savings Accounts (HSAs)

These accounts provide important benefits:

- Tax-deferred growth

- Potential tax deductions

- Tax-free withdrawals in certain cases

For example, Roth IRA contributions are made with after-tax income, but qualified withdrawals in retirement are tax-free. This can significantly improve long-term outcomes for younger investors expecting higher future income.

Many financial planners recommend maximizing employer retirement plan matches before investing elsewhere, as employer contributions effectively represent immediate returns.

Long-Term Investing and Market Volatility

One of the greatest challenges for investors is staying disciplined during periods of market turbulence.

Major declines occur periodically. The U.S. market has experienced several notable downturns over the past few decades, including:

- The dot-com crash (2000–2002)

- The global financial crisis (2008–2009)

- The COVID-19 market shock (2020)

Yet historically, markets have recovered and continued to grow over time.

Experienced investors typically approach volatility with a few guiding principles:

- Maintain a diversified portfolio

- Avoid panic selling during downturns

- Continue long-term contributions

- Review risk tolerance periodically

During the 2020 pandemic downturn, for instance, the S&P 500 fell more than 30% in early months but recovered to new highs later that year.

Real-World Examples of Long-Term Investment Strategies

Example 1: The Consistent Retirement Saver

A teacher begins contributing 10% of her salary to a 403(b) plan at age 25. She increases contributions whenever she receives a raise.

By maintaining consistent contributions and using low-cost index funds, she accumulates substantial retirement savings by her early 60s without relying on speculative investments.

Example 2: The Balanced Household Portfolio

A married couple in their 40s builds a portfolio consisting of:

- 65% equities

- 25% bonds

- 10% real estate funds

They rebalance annually and continue automated monthly contributions. This approach helps them pursue growth while controlling volatility.

Example 3: The Early Starter

A 22-year-old professional contributes $200 monthly to a Roth IRA invested in a total-market index fund.

Even modest contributions early in life allow compounding to work for decades.

Behavioral Discipline: The Often Overlooked Factor

Long-term investment success often depends less on strategy and more on behavior.

Research from Dalbar suggests that average investors frequently underperform the market due to emotional decisions such as panic selling or chasing hot trends.

Common behavioral pitfalls include:

- Selling during market downturns

- Buying assets after major price increases

- Trying to predict short-term market movements

Successful long-term investors typically follow a written plan and focus on fundamentals rather than daily headlines.

Evaluating Long-Term Investment Opportunities

When evaluating investments intended for long-term growth, experienced investors often consider several key factors.

- Cost structure: Lower expense ratios help preserve returns

- Diversification level: Broad exposure reduces risk

- Historical performance across cycles

- Tax efficiency

- Liquidity and accessibility

These criteria help ensure investments remain sustainable for long holding periods.

Common Questions Americans Ask About Long-Term Investing

What is considered long-term investing?

Long-term investing generally refers to holding investments for five years or longer, though many retirement strategies extend 20–40 years.

Is long-term investing safer than short-term trading?

While no strategy eliminates risk, longer holding periods historically reduce the impact of short-term market volatility.

How much should beginners invest monthly?

Many financial advisors suggest starting with 10–15% of income if possible, though even smaller contributions can be effective over time.

Are index funds better for long-term investing?

Index funds are widely used because they offer diversification, low costs, and competitive long-term performance.

Should investors adjust portfolios during market downturns?

Typically, investors rebalance rather than drastically change strategy unless their goals or risk tolerance change.

What role do bonds play in long-term portfolios?

Bonds provide stability and income, helping reduce volatility compared to equity-only portfolios.

How often should a portfolio be rebalanced?

Many investors rebalance annually or when allocations drift significantly from targets.

Can long-term investing work with small amounts?

Yes. Consistency and time are often more important than initial investment size.

Is it too late to start investing after age 40?

Starting later may require higher contributions, but long-term investing can still provide meaningful results.

What is the biggest mistake long-term investors make?

Emotional reactions to market movements often lead to poor timing decisions.

Viewing Long-Term Growth as a Financial Habit

Successful long-term investing is rarely dramatic. It tends to resemble a disciplined habit practiced over many years.

Regular contributions, diversified portfolios, and patience during market cycles form the foundation of most successful strategies. While no investment approach guarantees outcomes, history suggests that steady participation in the markets has been one of the most reliable ways to build wealth over time.

For many Americans, the key is not finding the perfect investment but maintaining the right habits consistently.

Key Insights for Long-Horizon Investors

- Long-term investing benefits from compounding over decades

- Diversification helps manage risk across market cycles

- Index funds remain a common foundation for growth portfolios

- Dollar-cost averaging reduces emotional decision-making

- Tax-advantaged accounts can significantly improve outcomes

- Consistent contributions matter more than perfect timing

A Long-View Perspective on Building Wealth

Long-term investing works best when it becomes part of a broader financial mindset rather than a short-term tactic. By focusing on diversified portfolios, consistent contributions, and tax-efficient strategies, investors position themselves to benefit from economic growth over decades. The most reliable advantage available to investors is often patience.

Snapshot Summary for Readers

- Long-term strategies rely on compounding and consistent investing

- Diversified portfolios help reduce volatility risk

- Index funds are widely used for cost-efficient exposure

- Tax-advantaged accounts improve long-term outcomes

- Behavioral discipline is often the deciding factor in success